Blockchain: Separating Fact from Fiction

Over the course of the past two years, blockchain has shown promise across nearly every industry—far beyond the confines of its cryptocurrency origins. The food industry is no exception, with key stakeholders like Walmart, Cargill, Tyson, Coca-Cola and Starbucks all announcing pilot programs this year.

Although blockchain has tremendous potential to speed up food recalls and enable the information transparency that consumers demand, there are important building blocks that must be in place before planning a blockchain implementation. Test your blockchain knowledge with these statements below to see if you can separate fact from fiction. Armed with the right information, you’ll be able to better understand the value of blockchain and how it fits into an entire ecosystem of data sharing before jumping immediately to its application.

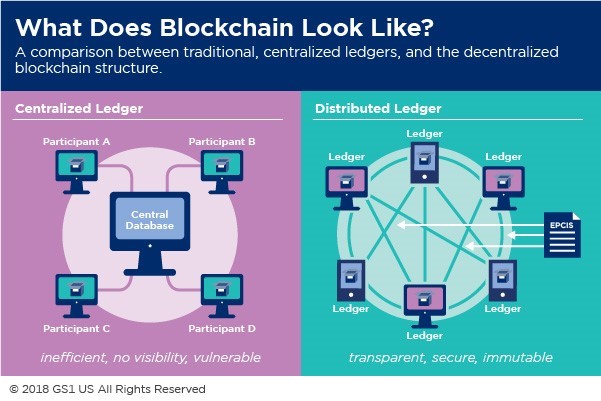

Blockchain is basically a shared database. This is true. While it’s no secret that shared databases have benefits, what makes blockchain special is that it is a distributed and immutable ledger. There is no single point of failure in a distributed ledger—it is a consensus of replicated and synchronized digital data geographically spread across multiple sites. This decentralized structure makes the data resilient to a technology or organizational failure.

Blockchain also supports “smart” supply chain contracts, meaning an automated execution of terms, conditions and business rules. Through this feature, trading partners can automatically enforce terms and conditions as previously defined, eliminating the errors and inefficiencies associated with the current manual processes based on legacy systems. A trading partner is prevented from writing a business transaction to the blockchain ledger that is outside of the rules specified in the smart contract. For retail grocery, this means far fewer item substitutions, more certainty around what is being shipped and when, and fewer discrepancies downstream.

Blockchain will do for the supply chain what email did for communication. This is also true—but Rome wasn’t built in a day. It will take time for blockchain to become a ubiquitous technology on par with email, and it is likely another decade away. However, given the amount of pilot programs underway, and the commitment from technology providers like IBM, Microsoft, and SAP to develop blockchain enterprise programs, many industry analysts believe blockchain will breakthrough to start to solve business process challenges in the next three to five years.

Purchasing blockchain software is all you need to create a traceability program. This is completely false! Industry stakeholders already leverage GS1 Standards, which enable traceability by ensuring all trading partners communicate in a uniform manner. Standards ensure systems interoperability, and provide a singular approach to creating, sharing and maintaining product information that supports, at the very least, “one up/one down” visibility of the product’s movement through the distribution channel. The internal data and processes a company uses to track products is integrated into a larger system of external data exchange that takes place between trading partners. Blockchain represents an opportunity for traceability to move faster—smart contracts and immutable ledgers expedite the flow of data between supply chain partners.

Blockchain can reduce food recalls from weeks to minutes. This is true, but only with a food traceability program already in place. Traceability has been achievable without blockchain, and many leading retailers have a long history working with farmers, distributors and processors on effective food traceability programs in order to assure consumers of food safety. Product recalls are significantly faster with standards in place to help break down any barriers caused by proprietary numbering systems and manual business processes.

Ultimately, now is the time to stay educated on blockchain and follow its development closely to uncover its many opportunities.

Related Articles

-

These not-so-innocent droplets of water must be managed in cold food processing facilities.

-

The technology may be the key to tracking and verifying foreign suppliers.

-

An evolution is coming.

-

Sharing the stories of foodborne illness and those impacted by it serves the industry in a critical way.